Right, let's get down to brass tacks. You’ve done the hard part—you’ve built an audience, put on a killer show, and your account balance is finally looking healthy. So, how do you actually get that money out of the platform and into your bank account where you can, you know, spend it?

It’s tempting to see this as a simple click-and-collect job, but choosing your payout method is a much bigger deal than it looks. This decision directly impacts how much cash you actually keep, how quickly you get paid, and how much of your personal info gets shared along the way.

Your Guide to Getting Paid from Cam Platforms

Navigating the world of streaming and stacking up your earnings is one thing. The final, and arguably most crucial, step is turning those digital tokens and tips into actual cash. This is the nitty-gritty, the business end of the job.

Picking a payout option isn't just about what's easiest; it's a strategic move. The perfect method for one creator could be a total nightmare for you. It's all a balancing act between a few key factors:

- Speed: Do you need the money tomorrow, or can you hang on for a week? Some transfers are almost instant; others take their sweet time.

- Privacy: Are you cool with the cam site’s payment partner showing up on your personal bank statement? For many, this is a massive deal-breaker.

- Fees: Let’s be real, nobody moves your money for free. You've got transaction fees, withdrawal costs, and currency conversion charges all lining up to take a slice of your hard-earned cash.

Why This Matters More Than You Think

Get this choice wrong, and you could be facing annoying delays, hidden fees that nibble away at your income, or privacy headaches you just don't need. A direct bank transfer, for example, is often fast and cheap, but it’s not exactly discreet. On the flip side, an e-wallet acts as a handy buffer, adding a welcome layer of privacy, but you’ll almost certainly pay more for the privilege.

Figuring out these trade-offs is what separates the pros from the newbies. It’s about managing your finances like a boss. To get a better feel for how these platforms tick, it’s worth checking out our guide on how webcam sites work.

In this guide, we’re pulling back the curtain on the most common payout methods out there—from old-school bank transfers to e-wallets and even crypto. We'll ditch the jargon and give you the straightforward, practical advice you need as a UK-based creator, so you can pick a method that protects both your money and your peace of mind.

Comparing Your Payout Options

So, you’ve hit your payout threshold. Nice one. Now for the crucial bit: getting that money into your hands. This isn't just a simple click-and-done; it's about picking the right tool for the job. Every payout method offered by cam platforms has its own personality—some are fast and cheap, others are discreet, and a few are just plain complicated.

There’s no magic "best" option that works for everyone. It all boils down to what you value most. Are you looking for lightning-fast access to your cash? Is keeping your financial life on the down-low your top priority? Or are you focused on squeezing every last penny out of your earnings by dodging fees?

Your answer will point you to the right method.

Payout Method Comparison at a Glance

To give you a quick overview, here’s a breakdown of the most common options available to UK creators. Think of this as your cheat sheet for making a smart decision.

| Method | Typical Speed (UK) | Average Fees | Privacy Level | Best For |

|---|---|---|---|---|

| Bank Transfer (FPS) | Minutes to a few hours | Very low to none | Low | Creators who want speed and low costs above all. |

| E-Wallets (Paxum, Payoneer) | 1-3 business days | Moderate | High | Those needing a privacy buffer from their bank. |

| Cryptocurrency (BTC, ETH) | Minutes to hours | Varies (can be high) | Very High | Tech-savvy creators focused on maximum privacy. |

| Prepaid Cards | Instant loading | High (multiple fees) | High | Ring-fencing cam income for daily spending. |

| Cheques | 1-2 weeks+ | Low | High | Anyone not in a hurry (and living in 1998). |

This table gives you the headlines, but the devil, as always, is in the details. Let's dig into what each of these really means for you and your money.

Direct Bank Transfers: The No-Nonsense Route

For most creators in the UK, a direct bank transfer is the go-to. It’s simple, familiar, and incredibly efficient, thanks to the Faster Payments System (FPS). This is the most direct path from the platform’s account to yours.

The biggest wins here are speed and cost. Request a withdrawal in the morning, and the money could be sitting in your account by lunchtime. Seriously, it's often that quick. Plus, the fees are usually rock-bottom or even zero, as it’s a standard, streamlined process for most platforms.

The trade-off, however, is privacy. While platforms are savvy enough to use discreet third-party processor names on your statement (it won't scream "SEXYCAMZ.COM"), it still creates a direct paper trail between their financial system and your bank. If you're comfortable with that, it's a brilliant option. But if you'd rather keep your cam work totally separate from your main financial records, you might want to look elsewhere.

E-Wallets: The Privacy Buffer

This is where e-wallets like Paxum and Payoneer really shine. These services are industry staples, acting as a financial middleman between the cam site and your personal bank account. They create a simple but effective privacy buffer.

Here’s the flow:

- The cam platform pays out your earnings to your e-wallet account.

- You then withdraw the funds from your e-wallet to your UK bank account.

The benefit is obvious: your bank statement just shows a payment from "Payoneer" or "Paxum," giving no clue as to its origin. But this layer of discretion isn't free. You'll often face a small fee to receive the money from the platform, another fee to withdraw it to your bank, and sometimes a currency conversion fee gets thrown in. These little cuts can add up, especially if you make frequent, small payouts.

The Reality of Fees: Imagine a £100 payout. You might lose £2 in a platform-to-wallet transfer fee, then another £3 for the bank withdrawal. That means you're left with £95. It’s a small percentage, but something you absolutely need to factor into your financial planning.

Understanding how these fees work is vital, especially if you're branching out. The payment structures for many OnlyFans alternatives operate on very similar principles.

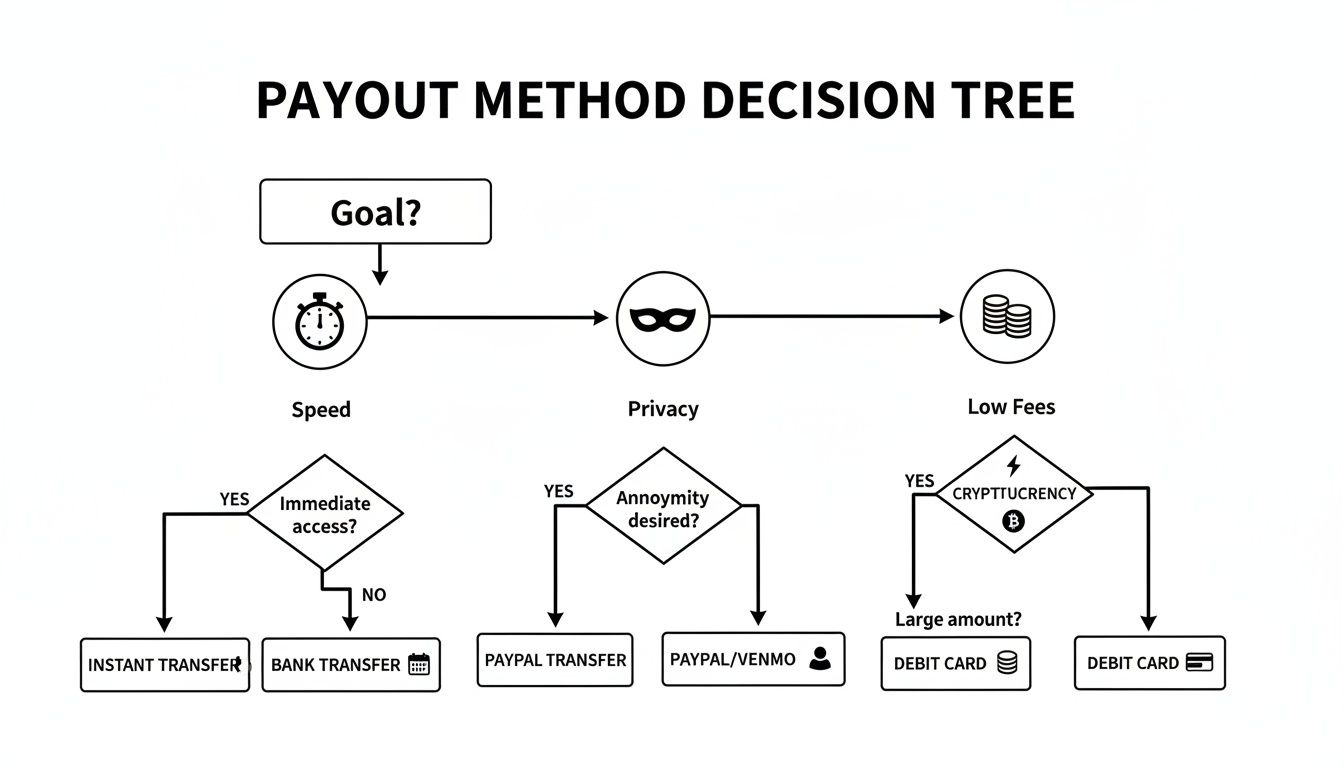

This decision tree helps you visualise the trade-offs you're making with each choice.

As you can see, if speed is your game, bank transfers are king. If privacy is paramount, e-wallets are your best bet. It's all about matching the method to your personal goals.

Cryptocurrency: The Wild West

Crypto is easily the most hyped-up payout option, but it's also the trickiest. Using currencies like Bitcoin (BTC) or Ethereum (ETH) lets platforms send you money with a high degree of pseudonymity. Your name and bank details aren’t plastered all over a public ledger.

While that sounds perfect for privacy, it's a double-edged sword. First, crypto isn't completely anonymous; skilled analysts can trace transactions if they really want to. The bigger issue for most creators, though, is volatility. The value of crypto can swing dramatically and without warning. A £500 payout in Bitcoin could be worth £550 or £450 by the time you convert it back to pounds.

You also need a bit of technical confidence. Setting up a secure wallet, understanding how to move coins, and selling them on an exchange all come with a steep learning curve. On top of that, network transaction fees (often called "gas fees") can sometimes be surprisingly high. Crypto is a powerful tool for those who get it, but it’s a risky gamble for newcomers.

Old School Options: Cheques and Prepaid Cards

Finally, a couple of old-school methods are still floating around, though they're becoming rarer. Physical cheques offer great privacy but are painfully slow—we're talking weeks to arrive and then more time to clear. Unless you enjoy the suspense, it’s probably one to avoid.

Prepaid debit cards are a more practical alternative. The platform loads your earnings directly onto a card they issue you. This is a fantastic way to keep your cam income ring-fenced for specific spending, but you have to read the fine print. Watch out for activation fees, monthly maintenance charges, and ATM withdrawal fees, as they can nibble away at your balance surprisingly fast.

A Closer Look at Direct Bank Transfers

For many creators in the UK, a direct bank transfer is the bread and butter of getting paid. It’s the most straightforward, no-fuss way to move your earnings from a platform straight into your personal account. No middlemen, no extra apps to download—just a simple, direct line for your cash. And it usually ends up being the quickest and cheapest option on the table.

Think of it like this: you finish a great session, hit your payout minimum, and request a withdrawal. Instead of that classic “3-5 business days” wait, the money can often land in your account within a few hours, sometimes even minutes. This is largely thanks to the UK's Faster Payments System (FPS), which most banks now use for near-instant transfers.

The speed of this system has been a real game-changer for creators who rely on a steady, predictable cash flow. The volume of Faster Payments transactions jumped by 14% in 2023 alone, making it one of the UK’s most popular payment rails. For streamers, this means cashing out daily tips almost instantly—a massive advantage when you've got bills to pay. You can dive into the full details in Pay.UK's recent summary.

The Unavoidable Privacy Question

So, if it’s so fast and cheap, why doesn't everyone use it? Well, the main catch is privacy. A direct bank transfer creates an undeniable paper trail between the platform’s payment processor and your bank account.

Let's be clear: the platform's explicit name will almost certainly not appear on your statement. Most use discreetly named third-party payment companies or holding companies to process payouts. Your statement is far more likely to say something bland like "Global Media Payouts Ltd" or "E-Payments Services UK."

Even so, the transaction is still there for your bank to see. While this isn't an issue for your day-to-day banking, it can become a factor in certain situations.

A Real-World Scenario: Picture this: you're applying for a mortgage in a couple of years. The lender will want to scrutinise your bank statements going back months. A steady stream of payments from a company they don't recognise might lead to awkward questions about your income source. It’s not necessarily a deal-breaker, but it’s something to be aware of if you’re planning major financial moves down the line.

Why Platforms Love Bank Transfers

From the platform's perspective, direct bank transfers are a dream. They’re reliable, highly secure, and carry a very low risk of fraud or chargebacks. This reliability is exactly why they often encourage creators to use this method.

Here’s why they’re big fans:

- Reduced Fraud: Bank transfers are difficult to reverse, which protects the platform from dodgy claims.

- Regulatory Compliance: It helps them meet their Know Your Customer (KYC) and Anti-Money Laundering (AML) obligations, as your bank has already verified you.

- Lower Costs: It's often the cheapest way for them to send large volumes of payments, meaning they can pass those savings on to you with lower (or zero) fees.

Because of these benefits, you’ll find that direct transfers are almost universally offered and are often set as the default payout option.

Is It The Right Choice For You?

Ultimately, a direct bank transfer is a fantastic option if your priorities are speed and keeping fees to an absolute minimum. It’s the workhorse of cam platform payout methods for a good reason.

However, if your main concern is creating a clear separation between your professional and personal finances, or if you just prefer not to have that link on your bank statement, then an e-wallet is probably a better fit. It’s a classic trade-off: you’re swapping a small degree of privacy for unparalleled speed and efficiency. For many, that’s a compromise worth making.

E-Wallets: Your Financial Middleman

If having a direct link between a cam platform and your bank account feels a bit too close for comfort, then e-wallets are your new best friend. Services like Paxum and Payoneer are mainstays in the creator world for one simple reason: they act as a financial buffer, putting a welcome bit of distance between your work and your personal finances.

Think of it like a digital PO Box for your money. Instead of a payment coming straight from the platform's processor, your earnings land safely in your e-wallet first. It's only when you decide to move the money to your bank that the transfer happens. The result? Your bank statement shows a generic "Payment from Payoneer," not a direct deposit from the platform. It’s a layer of discretion that many creators really value.

Of course, this extra privacy isn't free. It’s a service, and like any service, it comes with a price tag—usually in the form of small, ongoing fees that can chip away at your total earnings.

The Real Cost of Discretion

When you opt for an e-wallet, you need to get your head around the fee structure. It's rarely just one charge. You're likely to see a few different fees as your money makes its way from the platform to your pocket.

- Platform-to-Wallet Fee: Some sites charge a small fee, often just £1-£3, simply to send your payment out to your e-wallet.

- Withdrawal Fee: This is the big one. The e-wallet itself will charge you a fixed fee to move funds from their system into your UK bank account.

- Currency Conversion Fee: If the cam platform pays in USD but your bank account is in GBP, the e-wallet will manage the conversion for you—and take a percentage for their trouble.

Individually, these fees might not look like much, but they add up fast. Let's look at a realistic scenario.

The £100 Payout Example: You’ve earned £100. The platform takes a £2 fee to send it to your e-wallet. The e-wallet then charges another £3 to withdraw it to your bank. By the time that money hits your account, your original £100 is now £95. That's an effective 5% fee, which can make a serious dent over the course of a year.

It's About Discretion, Not Anonymity

There’s a common myth that using an e-wallet makes you completely anonymous. It doesn’t. These are regulated financial companies, which means they are legally obligated to verify your identity through a process called Know Your Customer (KYC).

You'll still need to provide official ID like a passport or driving licence, plus a proof of address, to get your account set up. The key difference is that you're sharing this sensitive info with the e-wallet provider, not with every single platform you work on. Your data is held centrally by Paxum or Payoneer, creating that crucial separation.

Where Does the Money Go Next?

Once your earnings are sitting in your e-wallet, you have a choice to make. The most common route is a simple transfer to your main bank account. However, many e-wallets also offer their own branded prepaid debit cards. This can be a clever way to keep your cam income completely separate for budgeting or spending.

In the UK, though, debit cards tied directly to a bank account are still king for online spending. This is part of a wider trend where debit cards make up a massive 48% of all online payments in the UK, which helps explain why so many platforms still focus on providing smooth bank and card payouts for British creators. If you're interested in the data, Airwallex's 2025 online payment analysis offers a great overview.

At the end of the day, e-wallets are an incredibly useful tool. They offer a practical solution for any creator who puts a premium on privacy. The trick is to go in with your eyes wide open, understand exactly what fees you’ll be paying, and decide if that buffer is worth the cost.

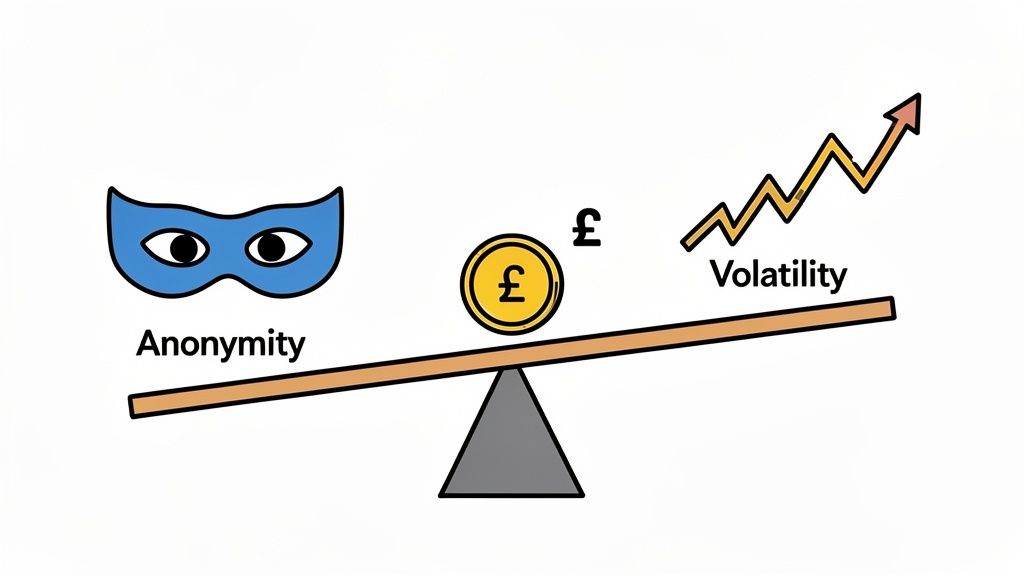

Navigating Crypto Payouts: Anonymity vs Volatility

Cryptocurrency is often sold as the holy grail for cam model payouts: total privacy, lightning-fast transfers, and a clean break from the traditional banking world. While there's some truth to that, the reality is a bit more complicated. It's less of a simple cash-out button and more of a high-stakes trade-off between anonymity and volatility.

First, let's clear up a huge misconception. Crypto isn't truly anonymous; it's pseudonymous. When a platform pays you in Bitcoin (BTC) or Ethereum (ETH), that transaction is permanently etched onto a public ledger—the blockchain. Your legal name isn't stamped on it, but the payment is tied to a unique digital wallet address. With enough digging, those digital breadcrumbs can sometimes be traced back to a real person.

The Volatility Gamble

The single biggest risk with any crypto payout is volatility. The price of cryptocurrencies can swing wildly, sometimes in a matter of hours. This means the value of your earnings is a moving target until you’ve actually converted it into pounds.

A Real-World Scenario: Let’s say you request a payout worth £500 in Ethereum. By the time it actually arrives in your wallet and you get around to selling it a day later, the market might have taken a nosedive. Your £500 could now be worth only £450. Of course, it could swing the other way and be worth £550, but it's a gamble you have to be comfortable with.

This unpredictability makes crypto a tricky choice if you're relying on your cam income for rent and bills. It demands a certain appetite for financial risk and the confidence to cash out quickly, minimising your exposure to those market swings.

Cashing Out and Paying Your Dues

Getting crypto out of a wallet and into your UK bank account isn't a one-click affair. It's a multi-step process.

- Set up a Crypto Wallet: First, you’ll need a secure software or hardware wallet to receive the coins from the platform.

- Choose an Exchange: Next, you'll need to sign up for a reputable crypto exchange that operates in the UK, like Coinbase or Kraken, and complete their full identity verification.

- Transfer and Sell: You then send the crypto from your personal wallet to your exchange account and sell it for GBP.

- Withdraw to Bank: The final step is withdrawing the pounds from the exchange directly to your linked UK bank account.

Each of these stages has its own learning curve and, often, its own transaction fees. And you can't forget about HMRC. Just because you were paid in crypto doesn't mean it’s invisible to the tax man. You are still legally required to declare these earnings on your Self Assessment tax return.

You’ll need to calculate the pound value of the crypto on the very day you received it, and that's the figure you'll pay Income Tax and National Insurance on. Keeping meticulous records isn't just a good idea—it's essential. Crypto offers a level of control that's hard to beat, but it forces you to become your own accountant and financial manager.

A Practical Checklist for Setting Up Your Payouts

Right, let's get down to brass tacks. Moving from theory to actually getting your money can feel a bit like filling out a mortgage application—a bit tedious and surprisingly personal. But trust me, taking the time to get this right from the start will save you a world of pain later. A single typo can send your earnings floating in cyberspace for weeks.

Think of this as your pre-flight checklist before you hit that cash-out button. Follow these steps, and you’ll ensure your hard-earned money has a smooth, direct flight into your account.

Before You Begin: The Essentials

First thing’s first: get your paperwork in order. Every legitimate platform and payment processor has to follow Know Your Customer (KYC) laws. It's not optional, and it’s there to protect everyone involved. You're almost always going to need:

- A valid government-issued photo ID: Your passport or driving licence is perfect. Just check that it’s still in date.

- Proof of address: A recent utility bill or bank statement (usually from the last three months) showing your full name and address will do the job.

It’s absolutely vital that the name on your ID, your proof of address, and the cam platform account all match exactly. Any little difference is an immediate red flag that will bring the whole process to a grinding halt.

The Step-by-Step Setup

Once you have your documents ready, the actual setup is usually pretty straightforward.

- Choose Your Payout Method: Head to the payments section of the site and pick your preferred option from their list—whether that's a direct bank transfer, an e-wallet, or something else.

- Enter Your Details Meticulously: Double-check, and then triple-check, every single digit of your bank account number and sort code. This is where most people trip up. A simple slip of the finger here is the number one reason for payment problems. You can find out more in our guide on how to avoid payout delays on cam sites.

- Submit Your Verification Documents: Upload clear, high-quality photos or scans of your ID and proof of address. If they're blurry or hard to read, they'll just get rejected, and you'll be back to square one.

- Enable Two-Factor Authentication (2FA): I can't stress this enough—this is critical. Switch on 2FA for both the cam platform and your payment service (like your banking or e-wallet app). It's the single best thing you can do to stop someone else getting their hands on your money.

A crucial tip: Never, ever use a shared or joint bank account for your payouts. It creates a messy paper trail and can lead to some very awkward conversations you’d much rather not have. Always use an account that is solely in your name.

If you have recurring earnings from subscriptions, you might appreciate the predictability of automated transfers. For instance, Direct Debits provided a stable income stream for many, accounting for a steady 10% of all UK payments in 2023. This method also gives you a clean, traceable record, which is brilliant for keeping your tax affairs in order and provides a reliable audit trail for HMRC. You can dig deeper into payment trends in the latest UK Finance report.

Your Cam Platform Payout Questions Answered

When you're dealing with the money side of camming, it's the little details that often make the biggest difference. Let's tackle some of the most common, practical, and sometimes plain frustrating questions that pop up when you're trying to get paid. Think of this as your go-to guide for sorting out the usual headaches.

How Often Can I Request a Payout?

This really depends on the platform. Some sites are super flexible, letting you cash out daily as long as you’ve hit a minimum balance, which might be something like £50. Others run a tighter ship with fixed weekly or bi-weekly payment schedules.

Your best move is always to dive into the 'Payouts' or 'Earnings' section of their terms of service to find out for sure.

A word of advice, though: cashing out small amounts every day might feel good, but it can get pricey fast. Always keep an eye on withdrawal fees. Cashing out £50 daily could easily cost you more in fees over a month than one single, larger weekly withdrawal. Creators with a big following can sometimes even negotiate better payout terms, so it never hurts to ask.

Will the Cam Site Name Appear on My Bank Statement?

Usually, no. Most of the big platforms are smart about this and use discreet third-party payment processors or generic corporate names to protect your privacy. What you'll see on your statement will likely be a very bland, unidentifiable company name that gives absolutely nothing away.

Here's a solid pro tip: always do a small test payout of the minimum amount first. This lets you see exactly what name pops up on your statement, giving you peace of mind before you start moving bigger sums. If total discretion is non-negotiable for you, an e-wallet is probably your safest bet.

What Should I Do If My Payout Is Missing or Delayed?

First things first: don't panic. More often than not, the culprit is something simple like a bank holiday or a tiny typo. Before you fire off an angry email to support, run through this quick mental checklist:

- Check the processing times: Have you factored in weekends and any public holidays? A payment requested on a Friday might not show up until Tuesday.

- Verify your details: Go back and double-check that your payment information is 100% correct. A single wrong digit in a sort code can send your money into a digital black hole.

- Contact support: If the normal waiting period has passed and you've confirmed all your details are right, it’s time to get in touch with the platform's support team. Give them your transaction ID, the date, and the amount requested. Most have a dedicated payments team ready to sort these issues out.

Do I Have to Pay Tax on My Cam Earnings in the UK?

Yes, absolutely. In the UK, any money you make from camming is considered self-employed income. This means you are legally required to declare it to HMRC by filing a Self Assessment tax return each year.

You’ll be responsible for paying both Income Tax and National Insurance on your profits. Keeping meticulous records of all your earnings and any business-related expenses isn't just a good idea—it's essential. We strongly recommend finding an accountant who has experience working with online creators to make sure you stay fully compliant and don't run into any trouble down the line.